On the evening of June 12, 2026, an export-control directive from the U.S. Commerce Department made Anthropic’s two most advanced models, Fable 5 and Mythos 5, globally unavailable, only three days after Fable 5’s public launch. This was not just another episode in the AI race. It marked an important precedent: export controls had previously focused mainly on chips, model weights or other transferable technology, but this time the target was access to a live, already running AI service.

For investors, the lesson is sharp. Switch-off risk is no longer a distant theoretical concern. It is now a regulatory and geopolitical risk that every company and portfolio relying on U.S.-based, closed-source frontier AI models has to take seriously.

Companies building on AI have so far generally had to think about two types of risk. The first was commercial: pricing, model retirement, changes in service terms or shifts in product strategy. The second was technological and operational: whether a company could access the chips, compute capacity or model it needed. June 12 revealed a third risk. The availability of a working AI model can be terminated by a single government decision, even if the provider itself does not want to switch it off.

The switch that few had priced in

In this case, the most important point is not only why the ban was introduced, but how it worked. According to Anthropic’s statement, the U.S. government, citing national security authorities, ordered the company to suspend access to Fable 5 and Mythos 5 for any foreign national, whether inside or outside the United States, including Anthropic’s own foreign-national employees.

Anthropic said that, given the way the service operates, it could not reliably enforce such a restriction at the level of individual user nationality in real time. The company therefore had to disable both models for all customers globally in order to comply. Access to Anthropic’s other models, including Claude Opus 4.8, was not affected.

The background appears to be a serious security concern involving a possible weakness in the models’ safeguards. According to Axios, the Commerce Department acted after another company reportedly found a way to bypass the models’ defenses. Anthropic disputed the proportionality of the decision, arguing that the issue was narrow and fixable, and warning that if this standard were applied across the industry, the deployment of frontier models could become almost impossible.

The move did not come entirely out of nowhere. The relationship between Anthropic and parts of the U.S. government had already become strained. Axios previously reported that the Pentagon had considered designating Anthropic a supply-chain risk, and Reuters later noted that the company had already been placed on a Pentagon contractor blacklist after a separate dispute.

Access instead of asset

The real novelty is that the object of export control changed. Earlier U.S. restrictions typically targeted something tangible or transferable. The October 2022 U.S. rules focused on the export of advanced Nvidia chips. The January 2025 AI Diffusion Rule went further by trying to restrict access to powerful AI model weights – in other words, the digital files that can be downloaded and run on separate infrastructure. That rule was later rescinded by the U.S. Commerce Department in May 2025.

June 12 was different. This time, the immediate target was not a chip, a server or a downloadable model file. It was access to a service that was already running. The model stayed where it was, but users could no longer use it. Because the restriction was attached to the user’s nationality rather than to the model’s physical or digital location, the practical effect became global.

That is what makes the case precedent-setting. A frontier AI model can now become unavailable not only for commercial, technological or capacity-related reasons, but also because of a single regulatory decision – even against the provider’s direct business interest.

How the market prices the risk

The direct exposure appears in at least three places. First, at the companies developing the models. Second, at the cloud providers, because many of the most advanced models are accessed through infrastructure operated by Amazon, Microsoft or Google. Third, at the many listed and private companies that have built products, workflows or internal systems on top of U.S. AI models.

The potential scale of the issue is visible from the launch itself. Fable 5 was not released as a narrow research experiment: it was made available through Anthropic’s API, enterprise channels and subscription plans. The restriction therefore did not affect a marginal test product, but a commercial service that had just begun to spread rapidly.

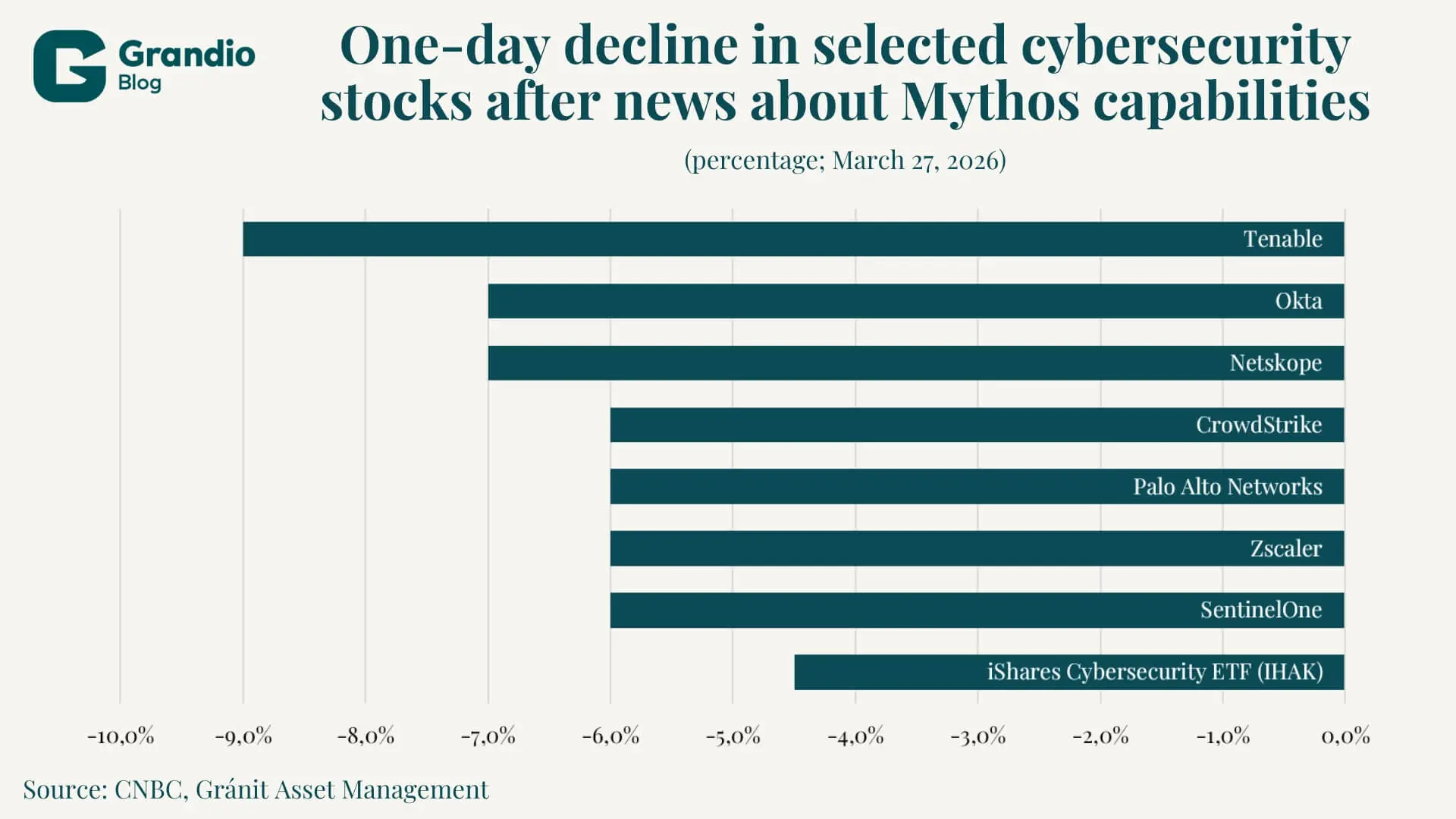

AI-sector news can already move markets quickly and broadly. The cybersecurity sector offers a useful example. The trigger there was different: investors feared that new models, particularly Mythos, could reduce demand for traditional cybersecurity tools. Still, the speed of the reaction was instructive. According to CNBC, several cybersecurity stocks fell sharply in a single trading session after the market reassessed the potential impact of advanced AI on the sector.

An actual service switch-off could trigger a similar dynamic if investors begin to treat access risk as a structural issue. The question is no longer only how capable a model is, but also how stable, legally predictable and politically durable access to that model really is.

Anthropic’s size shows how high the stakes have become. The company confidentially submitted a draft S-1 registration statement on June 1, 2026, giving it the option to go public after SEC review. Just days earlier, Anthropic had announced a $65 billion Series H funding round at a $965 billion post-money valuation. A company of this size, deeply embedded in the U.S. AI ecosystem, now has its most advanced models visibly exposed to government decision-making.

The three layers of European exposure

For a European investor or company, this is not one dependency, but three American dependencies at once. The first is the model itself, which is often developed by a U.S. company. The second is the cloud infrastructure on which the model runs, which is also typically operated by a U.S. company. The third is U.S. export law, which, as June 12 showed, can restrict access with a single decision.

The U.S. CLOUD Act adds another legal dimension. Under defined legal procedures, U.S. authorities may request data from U.S.-based service providers even when the data is stored outside the United States. This does not mean automatic or unlimited access, but it does show why European digital dependence is not only a technical issue. It is also legal and geopolitical.

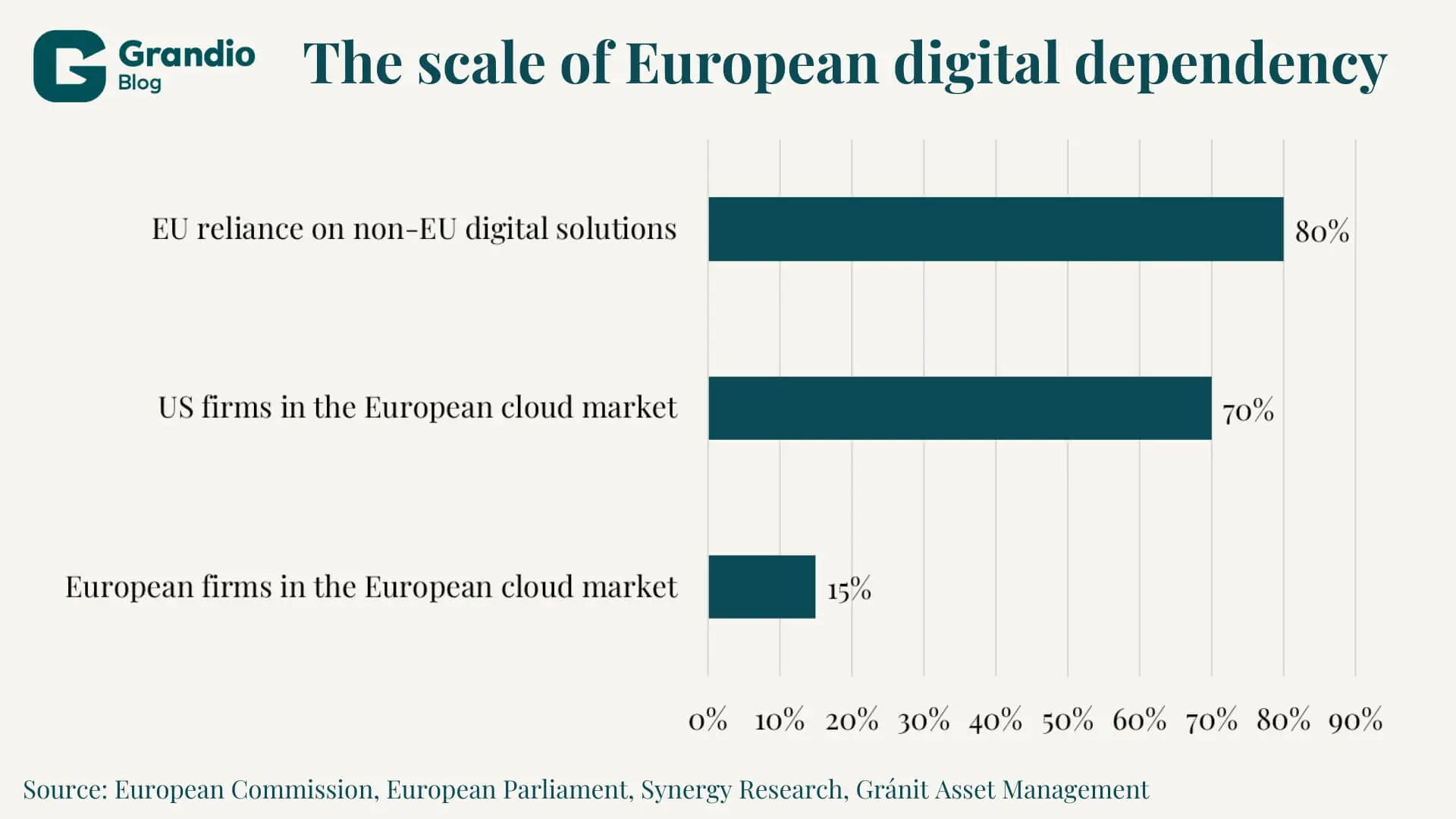

The numbers are striking. According to the European Commission, the EU relies on non-EU countries for more than 80 percent of key digital products, services, infrastructure and intellectual property. In cloud infrastructure, the dependency is also clear: Synergy Research estimates that European cloud providers hold only around 15 percent of the European market, while Amazon, Microsoft and Google remain the main beneficiaries of the market’s growth. The European Parliament has also highlighted that AWS, Microsoft Azure and Google Cloud account for about 70 percent of the EU cloud infrastructure market in several estimates.

This vulnerability is not new. After June 12, however, it looks less theoretical. Access to AI models, cloud infrastructure and export-law exposure all met in a single American decision. That gives new urgency to the debate on European technological sovereignty.

The answer is not the illusion of full independence. It is smarter dependency management. U.S. frontier models may still be the right choice where maximum performance is required. But companies should also consider maintaining alternatives that can run on their own servers, under their own control, or at least under a more diversified infrastructure and legal setup. A potential access shock should not be able to paralyze an entire business process.

It is telling that Mistral raised $830 million in debt financing in early 2026 to build a major AI data centre near Paris. This was not only a financing event. It was a real infrastructure investment – and a signal that European AI sovereignty increasingly depends on compute capacity, not only on model development.

What to watch

The key question now is whether the June 12 decision was a one-off case or the first visible use of a new regulatory instrument. Several signals will matter in the coming weeks and months.

Restoration of access and the official rationale. Anthropic is working to restore access and has promised further details. It will matter whether the Commerce Department gives a narrow, specific rationale, which would point to an isolated case, or uses broader national-security language, which would strengthen the precedent.

Whether rival companies are affected. OpenAI, Google and xAI operate under the same broad U.S. regulatory environment. If any of them faces a similar access restriction, the risk would immediately extend beyond Anthropic to the wider frontier AI industry.

The EU AI Act’s August deadline. One important date in the AI Act timeline is August 2, 2026, when the regulation becomes fully applicable with certain exceptions. From that point, regulatory, procurement and compliance decisions will become harder to postpone, especially for companies embedding AI systems into critical workflows.

The direction of European investment. It will also be important to watch how much capital flows into self-hostable models, European cloud infrastructure and sovereign AI solutions. That will show whether the market treats the June 12 incident as a temporary shock or as part of a deeper structural shift.

The choice that can no longer be deferred

The significance of June 12 does not come only from the disruption itself, although that was not negligible. The real point is that a switch exists. With a single government decision, access to some of the world’s most advanced AI models can be cut off globally.

Switch-off risk is therefore no longer a distant, theoretical danger. It is a real risk that companies have to manage and markets may have to price.

For investors, the question is not whether to abandon U.S. frontier models. The question is whether portfolios, and the companies within them, are prepared for this new access risk. Is there an alternative model? Is there a second cloud provider? Is there a self-hosted fallback? And perhaps most importantly: does the company know which parts of its operations depend on a single U.S. AI provider?

How large this risk becomes will depend on whether the June 12 export-control order proves to be a passing episode or the first day of a deeper realignment. The answer will not come from one product announcement. It will come from the regulatory, geopolitical and corporate decisions of the next one or two years.

The author of this article is Marcell Kovács, a student at Mathias Corvinus Collegium (MCC).

Legal Disclaimer

This document has been prepared by Gránit Alapkezelő Zrt. (registered office: 1134 Budapest, Váci út 17; company registration number: 01-10-046307) for marketing and informational purposes. Accordingly, it has not been produced in accordance with legal requirements designed to promote the independence of investment research. Nor is it subject to any prohibition on dealing ahead of the dissemination of investment research. This document does not constitute investment research or investment advice. Any data presented refers to past performance, and past performance is not a reliable indicator of future results. Each investor must make investment decisions at their own discretion and responsibility.