Following ReArm Europe and the 2025 Hague NATO summit, Europe is moving onto an unprecedented defense-spending trajectory. In the first round, this boosted traditional defense stocks, but in the background there are also AI-driven, software-led European defense scaleups, led by Helsing, Quantum Systems, Tekever, and ICEYE. The question is how much of the €800 billion envelope will flow to these new-generation companies, and whether the gap with American competitors will remain structural.

The €800 billion envelope is not a one-off stimulus, but a structural shift

The European Commission introduced the ReArm Europe/Readiness 2030 package in March 2025, aiming to mobilize up to €800 billion in defense funding by the end of the decade. One pillar of the package is the activation of the national escape clause under the Stability and Growth Pact, which alone could provide member states with up to €650 billion of fiscal space over four years. The other pillar is SAFE, a €150 billion EU loan facility whose funds can be used specifically for joint procurement from European manufacturers.

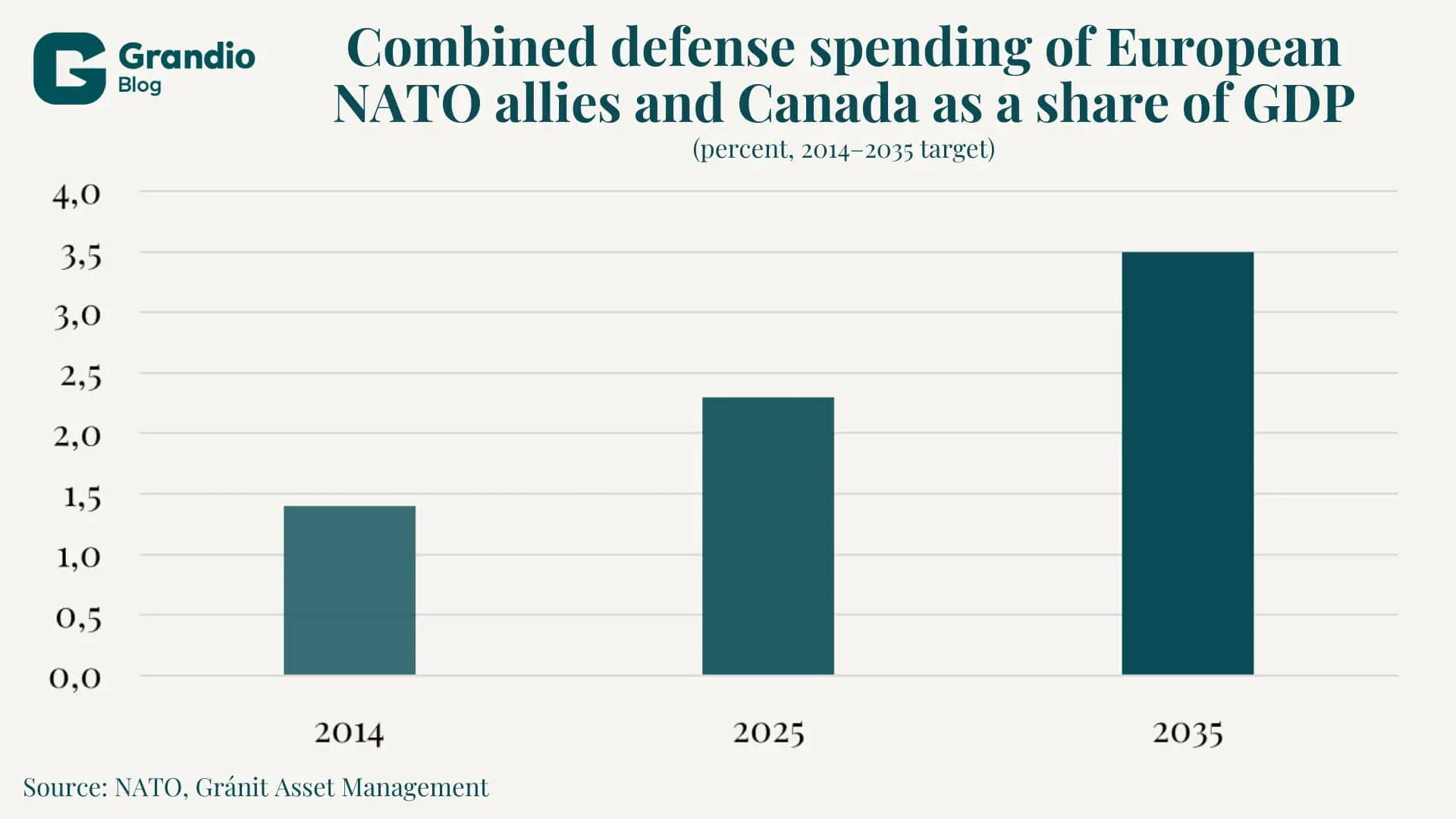

This is complemented by the closing document of the June 25, 2025 Hague NATO summit, in which member states adopted a defense spending commitment of 5 percent of GDP by 2035. Of this, 3.5 percent covers the direct defense budget, while 1.5 percent covers defense-related expenditure. According to NATO, the combined defense spending of European allies and Canada rose from 1.4 percent of GDP in 2014 to 2.3 percent in 2025, exceeding $574 billion in 2025. Reaching the 3.5 percent core target will therefore require multi-year budget growth, creating sustained demand pressure in the sector.

Equity markets, however, have largely already priced this in. According to McKinsey’s February 2026 analysis, European listed defense companies have delivered a 401 percent cumulative return since 2022, with most of that return generated since the 2025 Munich Security Conference. Rheinmetall’s 2025 revenue grew by 29 percent to €9.94 billion, its order backlog swelled to €64 billion, and the company expects another 40–45 percent expansion in 2026. The question, therefore, is where new capital flows from here.

The structural answer to the cheap-versus-expensive paradox: the neoprime companies

As seen in my previous article on cheap drones, one of the fundamental problems of modern warfare is that a $20,000–30,000 Shahed drone often has to be intercepted with a $4 million PAC-3 interceptor. There are two possible structural solutions to this problem: either the Western defense industry moves into the market for mass-produced, low-unit-cost products, or it shifts toward more advanced, AI-driven, multi-layered systems.

The classic primes — Lockheed, Raytheon, and their European counterparts — struggle to adapt, as Patriot replenishment takes 7–8 years, while new FPV drone designs appear almost weekly on the Ukrainian front. New capabilities such as autonomous drone swarms, real-time reconnaissance, AI-based electronic warfare, and space reconnaissance require a different industrial setup.

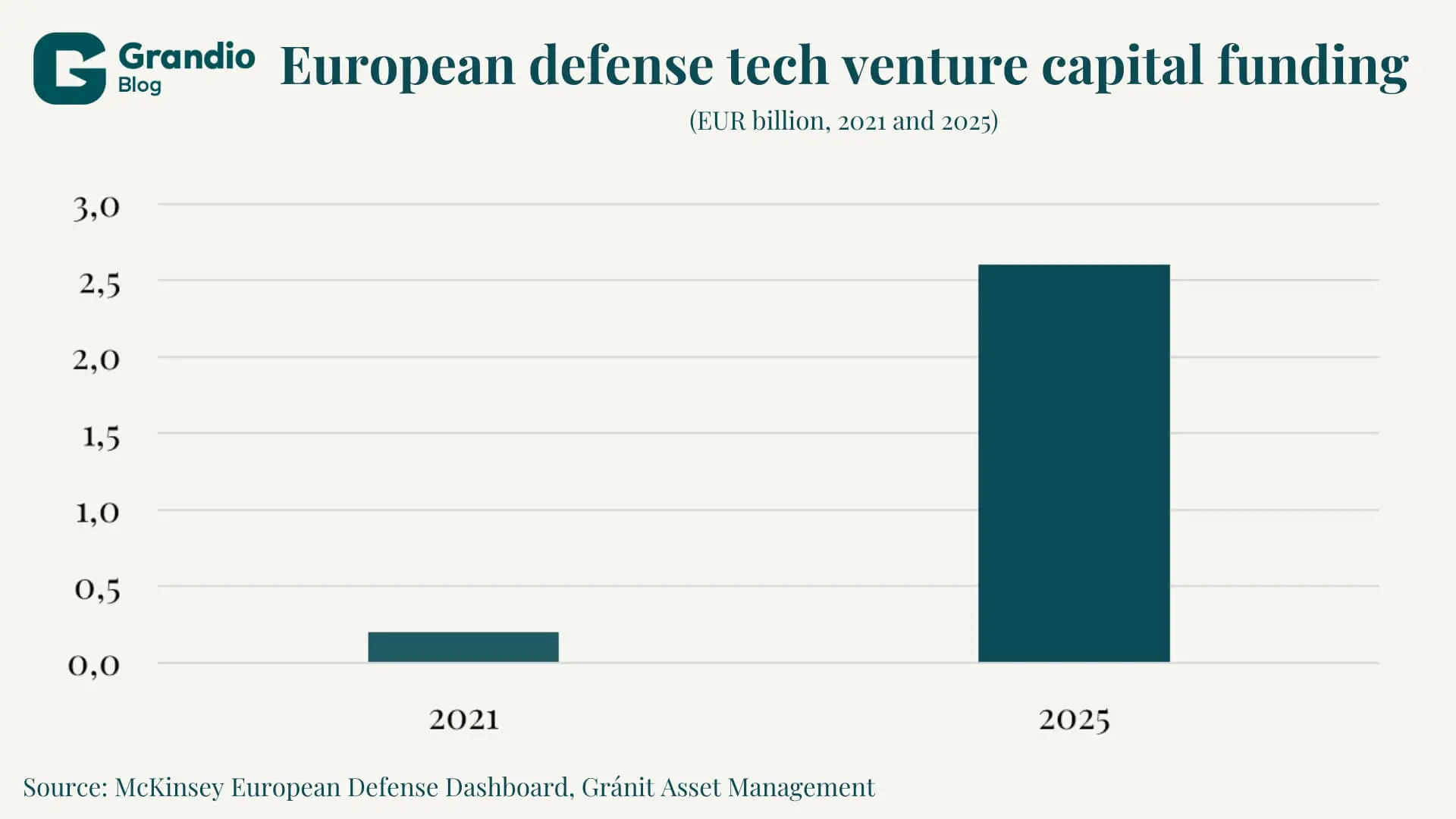

On the American side, the response has been the emergence of neoprime companies. According to PitchBook data, Anduril closed a $2.5 billion funding round in June 2025 at a $30.5 billion valuation, and has raised a total of $5.5 billion since 2022. Another major name in the field is Palantir. Europe has also developed its own version of the category: according to McKinsey, European defense tech venture capital funding rose from €200 million in 2021 to €2.6 billion by 2025, a thirteenfold increase in four years.

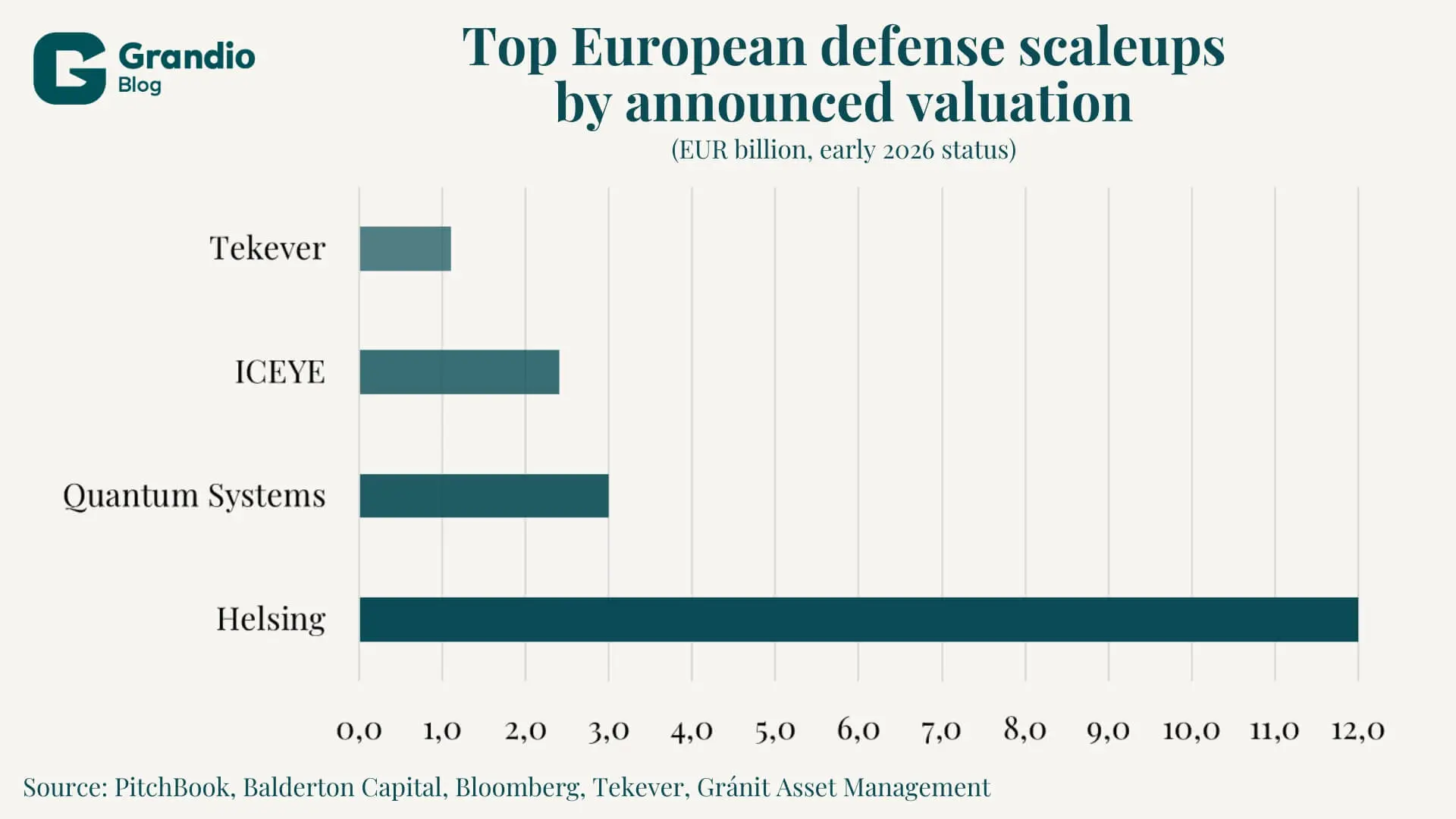

Helsing is the new €12 billion European flagship

The most prominent European neoprime company is Munich-based Helsing, which started as a defense AI software company in 2021 and closed a €600 million Series D round at a €12 billion valuation in June 2025. This more than doubled the company’s valuation in one year and elevated it into Europe’s five most valuable private tech companies. The round was led by Spotify founder Daniel Ek’s Prima Materia, with participation from General Catalyst, Lightspeed, Accel, and Saab, bringing the company’s total capital raised to approximately €1.36 billion.

Helsing won the contract for the AI backbone of the European FCAS, or Future Combat Air System, fighter program, which runs until 2070. The Bundeswehr ordered an initial €269 million tranche of HX-2 loitering munitions in February 2026. The company also delivers hundreds of HX-2s per month to Ukraine, with more than 4,000 units already on the front line. In June 2025, Helsing acquired Grob Aircraft and formed a partnership with Mistral AI to develop joint military models.

Quantum Systems and Tekever: the dual-use drone unicorns

Bavaria-based Quantum Systems became Europe’s first dual-use unicorn in May 2025 with a €160 million Series C round, before jumping to a €3 billion valuation in November after another €180 million round. Its total €340 million capital raise in 2025 was the largest move in the European dual-use sector among private companies, backed by Balderton, Peter Thiel Capital, Porsche SE, and Notion Capital. The company is not stopping there: it is targeting more than €500 million in revenue and an IPO in 2026.

One of Quantum’s most important moments came in December 2025, when, according to Bloomberg, it won a €210 million Falke reconnaissance drone contract from the German army. The order covers 520 unmanned aerial vehicles, with an option for an additional 500 units between 2027 and 2032.

Portuguese Tekever is on a similar trajectory. The AI-driven drone manufacturer reached a valuation above £1 billion, or approximately $1.25 billion, in May 2025, and simultaneously announced a £400 million, five-year British development program called OVERMATCH. Tekever’s AR3 and AR5 drones have already completed more than 10,000 combat flight hours on the front lines in Ukraine. The investment round was led by Ventura Capital, with participation from Baillie Gifford and the NATO Innovation Fund.

ICEYE: the satellite reconnaissance player that reached profitability

Finnish ICEYE is building a satellite constellation that uses synthetic aperture radar, or SAR, to take high-resolution images at night and through clouds. In December 2025, it closed a €150 million Series E round led by General Catalyst, at a €2.4 billion valuation. It reached profitability in 2025, doubled its revenue to more than €200 million, put 25 new satellites into orbit, and is targeting a production pace close to one satellite per week in 2026.

The high point of 2025 for ICEYE was the SPOCK 1 contract, won within the framework of a joint venture with Rheinmetall. Under the contract, the German army ordered sovereign SAR radar satellite constellation systems with a gross value of €1.7 billion on December 18, 2025, running until 2030 and also including extension options. Rheinmetall ICEYE Space Solutions, a 60/40 joint venture between Rheinmetall and ICEYE, primarily supports reconnaissance for the German brigade deployed to Lithuania. ICEYE has a large government customer base, with Polish, Finnish, Dutch, and Portuguese contracts, as well as a smaller but growing civil business.

The Europe–US gap and the role of the SAFE facility

These numbers need to be viewed against a benchmark. According to McKinsey, American defense tech venture capital in 2025 was roughly three times the level seen among European NATO allies, while 40–50 percent of capital in European growth and late-stage rounds also came from American investors. Anduril alone absorbed nearly one-third of global defense tech venture capital between 2022 and 2025.

This may be offset by the EU’s SAFE public procurement rules, which require a 65 percent EU/EFTA/Ukrainian share and exclude companies under third-country control. This is a European preference clause that softens the advantage of American suppliers, but it also raises serious questions for scaleups such as Helsing, Quantum Systems, and ICEYE, whose ownership structures include significant American investor stakes.

The V4 and Hungarian angle: strong traditional defense industry, limited scaleups

The Hungarian and V4 angle has two sides. On the traditional prime side, the region already has an established position. Rheinmetall Hungary Zrt. — 51 percent Rheinmetall, 49 percent Hungarian state — manufactures the Lynx KF41 infantry fighting vehicle in Zalaegerszeg under a 209-unit contract with the Hungarian Defence Forces. Rheinmetall also announced further investment in October 2025 for the development of the Panther KF51 main battle tank. In Várpalota, a 30-millimeter ammunition plant has been operating since July 2024 as a joint investment between Rheinmetall and the state-owned N7 Holding. Poland, meanwhile, leads the region with defense spending equal to 4.7 percent of GDP, and in May 2025 ordered three ICEYE SAR satellites for €200 million under the MikroSAR program.

On the scaleup side, however, Hungary’s presence remains modest. In November 2025, Hungary submitted its plan for a €16.2 billion, or approximately HUF 6,300 billion, SAFE loan envelope, which, alongside cohesion funds, is one of the country’s largest mobilizable funding frameworks. Actual allocation will begin in early 2026, meaning this is the moment for the Hungarian defense industrial ecosystem to position itself. The consolidation of the 4iG Group and N7 Defence in June 2025 is a step in this direction, but a Hungarian scaleup on the scale of Helsing or Quantum is still missing from the market. The SAFE framework therefore offers an opportunity for suppliers alongside Rheinmetall and other primes, while also creating urgent pressure on the domestic ecosystem to emerge as an independent systems integrator.

Investor risks: where not everyone is a winner

Several risks are present in the market. The first is the size of valuations: Helsing’s €12 billion valuation is 50–60 times its revenue, so any geopolitical de-escalation could trigger an immediate correction. Second, dependence on government contracts comes with extreme concentration. A good example is Quantum’s Falke contract, which alone accounts for nearly three-quarters of expected 2025 revenue.

Third, the possibility of a successful exit is extremely narrow in the defense industry. On the European side, every such scaleup has remained private so far, and ICEYE’s potential 2026 IPO would be the first major turning point in this regard, as well as a major public test for the European industry. Finally, battlefield performance remains decisive. According to some reports, Helsing’s HX-2 drone showed a declining hit rate in late 2025 against increasingly sophisticated Russian electronic warfare, indicating that combat experience does not eliminate efficiency risk and that constant innovation is required.

Five metrics worth tracking for defense scaleups

Beyond classic industry performance indicators, the following five metrics can help investors quickly assess the viability of a European defense scaleup.

Government-backed order backlog and the share of multi-year framework contracts

The growth trajectory stands or falls on multi-year framework contracts, not one-off projects. Helsing’s FCAS and Bundeswehr contracts, ICEYE’s €1.7 billion SPOCK 1 framework, and Quantum Systems’ 2027–2032 Falke options demonstrate exactly this. At the same time, a multi-year contract concentrated with a single buyer is also a serious concentration risk.

Capital efficiency relative to the American benchmark

Anduril reached a $30.5 billion valuation with approximately $5.5 billion of capital raised, or roughly 5.5x. Helsing reached €14 billion from €1.36 billion, or around 10x, while Quantum Systems reached $3.5 billion from just $410 million, or around 8.5x. Higher capital efficiency is a good sign in itself, but if fundraising capacity is weaker than that of American competitors, it can become a long-term growth disadvantage.

Share of dual-use revenue

Companies manufacturing dual-use equipment, such as Quantum Systems and ICEYE, are more resilient to defense spending cycles because they also generate civilian revenue. ICEYE, for instance, diversifies through insurance damage assessment and deforestation monitoring, which could sustain growth even in the event of a potential 2027–2028 rearmament plateau. A civilian revenue share above 30 percent is already considered healthy.

Production capacity and iteration cycle

It is worth monitoring ICEYE’s pace of one SAR satellite per week, Helsing’s delivery of several hundred HX-2 drones per month, and Quantum Systems’ output of several thousand drones per year. These figures show whether a company can truly perform at neoprime scale, or whether it remains in the prototype phase. The 5–8-year production lead times of classic primes represent a competitive disadvantage against the 6–12-month iteration cycle of scaleups.

Exit potential: IPO or strategic acquisition

In the European venture market, exit has remained an open question for years. ICEYE’s potential 2026 IPO and Helsing’s expected listing around 2027–2028 serve as direct investor indicators. If such companies truly manage to go public in Europe, that would be positive not only for the individual companies, but also as a sign of maturity for the entire ecosystem.

Closing thought: structural transformation comes after the classic rally

The 2025 defense stock rally has largely already played out. The pricing of Rheinmetall, Saab, and Leonardo reflects past performance and expected growth over the next 2–3 years. The next major opportunity is likely to be found among defense scaleups, where the key question is what proportion of the €800 billion ReArm Europe envelope and the NATO 5 percent target will flow to these neoprime companies.

If the SAFE 65 percent EU share requirement, the emergence of European exit opportunities — ICEYE in 2026 and Helsing potentially in 2027–2028 — and stronger M&A between classic primes and scaleups occur together, then by 2027–2028 Europe could build its own Anduril, or even a competitive field made up of several such companies. If, however, this structural transformation fails to materialize, a significant share of the €800 billion envelope will be implemented using American or Israeli technology, and Europe’s strategic autonomy in defense technology will remain an illusion.

From an investor perspective, the next 12–24 months will be the truly decisive period, and it is worth watching both the listed primes and the private scaleup layer at the same time.

The author of this article is Marcell Kovács, a student at Mathias Corvinus Collegium (MCC).

Legal Disclaimer

This document has been prepared by Gránit Alapkezelő Zrt. (registered office: 1134 Budapest, Váci út 17; company registration number: 01-10-046307) for marketing and informational purposes. Accordingly, it has not been produced in accordance with legal requirements designed to promote the independence of investment research. Nor is it subject to any prohibition on dealing ahead of the dissemination of investment research. This document does not constitute investment research or investment advice. Any data presented refers to past performance, and past performance is not a reliable indicator of future results. Each investor must make investment decisions at their own discretion and responsibility.